Upcoming Event

Industrial real estate sector closes Q3 with strong fundamentals

Jessica Perry//October 10, 2022//

Rounding the corner on 2022, the industrial real estate sector closed the third quarter with strong fundamentals. The vacancy rate is under 3% while rents continue to grow as demand refuses to abate, despite potentially brewing economic headwinds. In the region, that differs slightly from the national picture where Cushman & Wakefield reported industrial supply outpaced demand for the first time in eight quarters.

But that isn’t the case in New Jersey.

Here, net absorption and demand are still neck and neck. Despite construction, fierce demand keeps preleasing strong with about 90% of under-development product spoken for. “As of yet, we have not seen the uncertainty in the national economy directly impact the imbalanced supply and demand curve found in our region,” said James Delmonte, vice president and director of research at NAI James E. Hanson.

“It’s the diversity of demand that is so key,” JLL Vice Chairman and Head of the Northeast Industrial Region Robert Kossar told NJBIZ just ahead of the close of Q3. “Industrial isn’t just e-commerce these days. Everyone’s trying to right-size their supply chain. Everybody’s trying to get closer to the customer, which goes super well for New Jersey.” On top of that, Kossar added that compared with most states, New Jersey has a “good labor story,” as well, which is becoming increasingly important to occupiers.

“[I]t doesn’t matter if you’re a brick-and-mortar store of a manufacturer, or any kind of wholesaler — it doesn’t matter what you do right now. You’re trying to expand your inventory because you don’t want to get caught without products and you’re wanting those products to be closer to the customer,” he said. “[W]hether they’re an appliance manufacturer and wholesaler or a retailer with physical brick-and-mortar stores and e-commerce, or a medical device manufacturer that needs to distribute locally. I mean, they’re all active right now.”

Construction is also on the upswing. According to JLL’s Q3 Industrial Insight, building is at “its highest level in history,” with approximately 27.2 million square feet under development – double that of 15 months ago – and 17.7 million square feet having broken ground in the Garden State year to date. According to NAI Hanson’s 3Q 2022 Industrial Report, 16.5 million square feet of new construction is expected to be delivered over the next five quarters across North and Central Jersey.

For now, the north leads the way, with the Ports – and its 1.8% vacancy rate – still seeing the most activity, boasting the highest rentable building area (5.2 million square feet) under construction, according to NAI Hanson. Following that was Exit 10/12 with a 1.6% vacancy rate and 3.2 million square feet RBA under construction, reflective of an inevitable change in focus due to space constraints. JLL reported the highest concentration of new development is in Central Jersey, where construction is up nearly 40% over last year.

Kossar said that beyond demand, rental increases still warrant all that development. In its Q3 report, JLL found asking rents were up 34% for the past 12 months for an average total asking price of $15.56 per square foot. “Because construction pricing has increased so significantly with inflation,” Kossar said, “the landlords also need those higher rents in order to make the deals work.”

Most submarkets across the state have seen their average asking rents pass the $10 threshold — except for Exit 7A and Warren & Sussex, which posted rates of $9.03 per square foot and $8.02 per square foot, respectively, in Q3. That distinction is unchanged from the second quarter of 2022; but the rates are both up from that period’s $8.67 per square foot in Exit 7A and $7.44 in Warren & Sussex.

Race for space

The low rents around Exit 7A offer both appeal and opportunity. The submarket was included in a group of three identified by NAI Hanson as being on the receiving end of 70% of the under-construction square footage that will be delivered over the next five quarters. And the vacancy rate there is higher than the statewide average, the firm reported, at 2.7%.

Kossar said that despite headwinds and “the sort of negative press around some of the occupiers, our tenants to market continues to increase.”

Inevitably, developers and tenants are pushing the boundaries of where they’ll settle to gain access to, well, the access New Jersey affords for moving goods to where they need to go. According to NAI Hanson’s Delmonte, “Tenants are still being forced to expand their search beyond the historically popular submarkets which has continued to drive up the record-high rates we’re seeing in locations such as the Exit 8A submarket.” While noting the market could cool down in the months ahead, he pointed to “unprecedented demand from e-commerce and big box retailers” as driving forces.

Kossar said he expects the southern and western parts of the state will continue to do exceptionally well, especially moving forward, because they have to. “There’s no more, there’s very little opportunity in the infill and that infill opportunity is very expensive.” For example, the JLL report shows average asking rents in the Meadowlands ($22.02 per square foot) and Port ($21.31) as well above the statewide average.

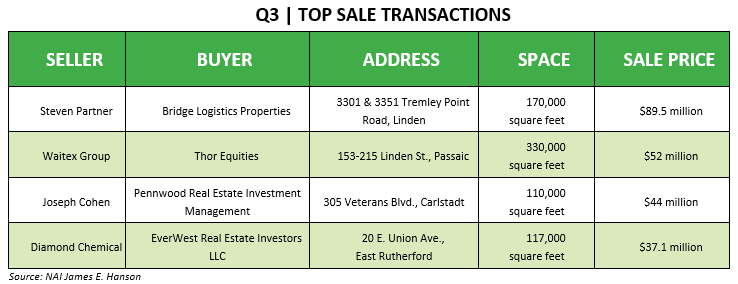

Those rising rents served to reinforce investment over Q3. The biggest sale of the quarter, according to NAI Hanson, was Bridge Logistics Properties’ purchase of a 170,000-square-foot site in Linden for $89.5 million. The firm reported more than 2.8 million square feet of space traded in the sector over the quarter, with capitalization rates steady in the low-to-mid 5.0% range.

“Rates are up, capital is up. And as a result on the acquisition side, it’s really affecting development sites,” Kossar said, pointing out the relationship between the capital markets and the underlying fundamental market. “And then on stabilized assets getting sold, many of the players are sort of on the sidelines … who were so active over the past two years.”

Though things do have the potential to slow slightly due to outside pressures, because vacancy is so limited statewide, JLL said that any potential increase would still maintain a landlord favorable environment.

And as Kossar pointed out, “[If] the deals don’t work, they’d just as soon not lease the space. So, I think everybody’s sort of in a good spot to have continued upward momentum.” And even if it’s not as good as the past couple of years, he said “it’s still in a really good place.”